![How to Switch Banks [6 Ways to Get Started]](https://blog.qubemoney.com/wp-content/uploads/2020/09/how-to-break-up-with-your-bank.jpg)

Your bank plays a crucial role in your life and deciding to switch banks isn’t easy.

Whether you use a bank for your daily money transactions or manage your retirement savings, banks keep your finances in order. With all the banking options available, you can switch to a bank that suits your needs.

Even with the abundance of options available, many consumers choose to stay with their current bank out of complacency. But this isn’t a reason for you to stay put.

If your bank isn’t making your financial life easier or not meeting your expectations, you may want to switch banks. In this post, we’ll provide a few reasons why you should switch banks as well as a step-by-step guide on how to switch banks.

Related: Digital Banking: Strengths & Weaknesses of Online Digital Banks

WHY YOU SHOULD SWITCH BANKS

There are plenty of reasons to switch banks. Whether you’ve experienced poor customer service, pay high maintenance fees, or you don’t like your bank’s vibe, find an institution that fits your needs.

If any of the following reasons apply to your situation, switching banks might make sense.

YOU HAVE TO LEAVE YOUR HOME TO COMPLETE TRANSACTIONS

Fewer and fewer people are visiting a physical bank location. During the global pandemic, bank branch visits fell 30% in April.

With many bank customers seeking the ease of online banking, it’s no surprise the convenience of accessing your bank right from the comforts of your home makes online banks more attractive.

Not only do many fintech banks offer access to their bank right from your fingertips, but many provide a virtual experience for their customers. Whether you want to access a bank representative to resolve a banking issue or access online tools to get your budget on track, you deserve a bank that gives you an exceptional online banking experience.

Online customer service features you may want to look for:

- An exceptional mobile banking experience

- Customer support available via phone

- Other online tools and budgeting and personal finance management resources

- Quality chat support

Everyone has plenty of frustrations in their lives, you don’t need your bank adding more. If your bank doesn’t provide an excellent digital experience, it’s time to consider other banking options.

YOUR BANK IS STUCK IN THE DARK AGES

Though many internet-only banks continue to adapt to new technology and banking innovation, others are stuck in the dark ages. Again, since online banking is becoming more popular each day, your bank should allow you to access a variety of features right from your device. If your bank isn’t affording you these luxuries, it might be time to switch.

Features you might want to look for in a new bank:

– Online/mobile banking

– Budgeting tools

– Subscription controls

– Roundup technology

– Spending reports

– Receipt capture

– Transaction notes

– Bill pay

– Peer-to-peer transfers

– Mobile deposit

– Geotracking

– High-yield accounts

-Joint accounts

-Teen and kid cards

– Payday 2 days early

Although this list may appear daunting at first glance, it speaks volumes to how far banking tech has come. If this doesn’t get you excited about what’s to come in the banking industry, you may want to read it again!

From automatic savings to early paydays to modern user experience, many banks are continuing to innovate their products and services to meet the unique banking needs of consumers.

With this in mind, you may take a look at Qube Money, a digital banking solution committed to rolling out all these technologies to make it easier for you to manage your finances.

YOU’RE PAYING TOO MANY FEES

Most banks have overdraft fees, maintenance fees, return deposit fees, stopped check fees, ATM fees, and more. In today’s digital world, you shouldn’t be paying banking fees.

Why pay $30 for an overdraft fee when the technology exists to prevent overdrafts?

Why pay for a stopped check, when technology automates it?

Review the fees at your bank and compare them to other financial institutions. You might be surprised how much you’re paying and decide to reevaluate your bank of choice.

Digital banks eliminate many of the above-mentioned fees while also providing the latest tech in the banking world. For instance, Qube Money’s basic account is a fee-free account, period.

YOUR BANK ISN’T HELPING YOU IMPROVE YOUR FINANCES

From saving retirement to becoming debt-free, there are plenty of financial goals you may want to achieve. But, it’s easy to let life get in the way and veer you off course of the pursuit of your financial goals. Thus, working with a bank that can improve your finances is worth its weight in gold.

For example, let’s say your financial goal is to become debt-free in the next five years. Staying motivated and consistent is an uphill battle, which keeps many consumers in the debt cycle year after year.

To rid yourself of debt, many banks, like Qube Money, may offer debt elimination tools that can give you the extra motivation and guidance you need to achieve your goal once and for all.

If your bank doesn’t offer tools and resources to help you improve your finances, there are other banks available that do. Trying to achieve your goals alone may leave you feeling frustrated and defeated. Working with a bank that helps you better manage your finances in any capacity may give you the financial confidence you need to achieve any money goal you set.

YOU’RE NOT EARNING INTEREST

Most banks offer minimal interest rates on savings. According to the Federal Deposit Insurance Corporation, the average interest rate for savings accounts is 0.06%. While this is the benchmark for the rate environment, it’s not something you may want to settle for.

To make your money go further, it’s wise to switch to a bank that has high-yield savings or checking accounts. Many virtual banks have interest rates well above the national average, making them more appealing to consumers.

While you may find rates between 0.01% and 1.25%, the variations in rates can make a big difference. For example, let’s say you deposit $10,000 in two different savings accounts and keep it in there for 12 months without adding any funds. One savings account has an interest rate of 0.1%, and the other has an interest rate of 1.25%.

Assuming interest compounds monthly, the savings account with a 1.25% APY will come to $10,125.72. In comparison, the savings account with the 0.1% interest rate will have $10,010.00 after one year of monthly compounding interest, you’ve earned $116 more with the higher interest savings account. Throughout a lifetime, this interest can help your money grow.

If you have the opportunity to help your money grow, why not take advantage of it?

HOW TO SWITCH BANKS

Now that you’ve decided to switch banks, use these steps to ensure your finances stay intact while you transition. These steps will make sure the process is seamless.

FIND A NEW BANK

Before you do anything, make sure you compare all your options and find the best bank that suits your financial needs. For example, if you need help budgeting, using technology like Qube Money’s digital cash envelopes can help you get your finances on track and reach your financial goals with ease.

Be sure to compare fees, interest rates, features, accessibility, and customer service experiences to decide which bank makes the most sense for your unique financial situation.

OPEN AN ACCOUNT AT YOUR NEW BANK

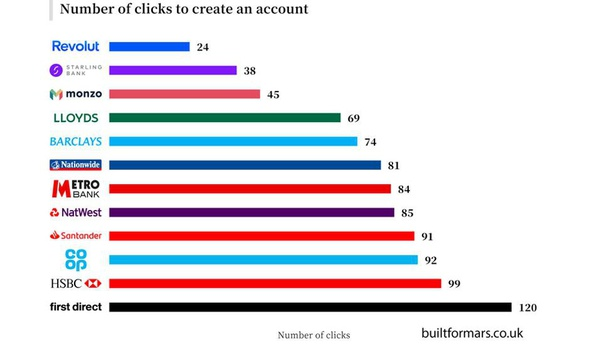

Once you decide on a bank, open a new account. Most banks make opening a new account a straightforward and fast process. Don’t worry about this step taking up too much of your time. Banks with good tech take a matter of minutes to open an account.

For example, here’s a list of UK banks that shows the number of clicks it takes to make an account. New banks are focused on decreasing the number of clicks it takes to create an account.

Make sure not to close your existing account. You’ll want to wait until you’ve confirmed you set up your account correctly.

MOVE DIRECT DEPOSITS AND AUTOMATIC BILL PAY

If you have automatic payments coming out of your old accounts, you should cancel them. However, make sure to take the time to write down all of the information so you can set them up with your new account.

Contact your employer to change your direct deposit to your new account.

TRANSFER ACCOUNT BALANCE

Once your direct deposit is established, and you’re paying bills, you’ll want to transfer your funds from your old account to your new account. Many banks may provide a check while others will do an ACH transfer. Either way, make sure to transfer the entire account balance to your new bank account.

CLOSE THE OLD ACCOUNT

If you manage bills through your old account, it’s wise to redirect them to your new account before you cancel it. It’s easy to forget a bill or other expenses during your transition. Monitor both accounts to ensure you’ve transferred everything before canceling.

Depending on your bank, you might need to go into a bank branch or sign a document to close your account.

EXPLORE YOUR NEW BANK FEATURES

The heavy lifting is behind you, and it’s time to implement all of the new features your bank offers. Whether they have a banking app or various budgeting tools, it’s time to put all of these features to the test, using them in your daily life.

The more comfortable you become with your new banking features, the more you can utilize them and take advantage of their functionality to make your daily banking life easier.

Breaking up with your bank might be a challenge. Whether you don’t enjoy change or don’t want to spend the time and effort making a move, switching banks can be a daunting task.

But, banks play a significant role in your financial well-being. You should switch to a bank to help you reach your financial goals and create strong money management habits.

If you don’t enjoy your current banking experience or feel bombarded with fees, it’s time to switch banks. Prioritize your financial needs and start comparing your options today.

{kind=link}